This text continues to characterise Poles’ travels abroad. The analysis is still based on the results of the study described in Travel Search Trends 2020. Part 1 – characteristics of the respondents conducted on a group of respondents by the Qtravel travel agency. It was a pilot study, the results of which cannot be applied generally to the entire population (it included mainly people that used the services of online travel agencies). However, given the systematically growing group of tourists who use OTA services (on-line travel agencies), the trends that characterise this form of shopping can be considered as a manifestation of transformations that are permanently taking place in tourism and the demand for it.

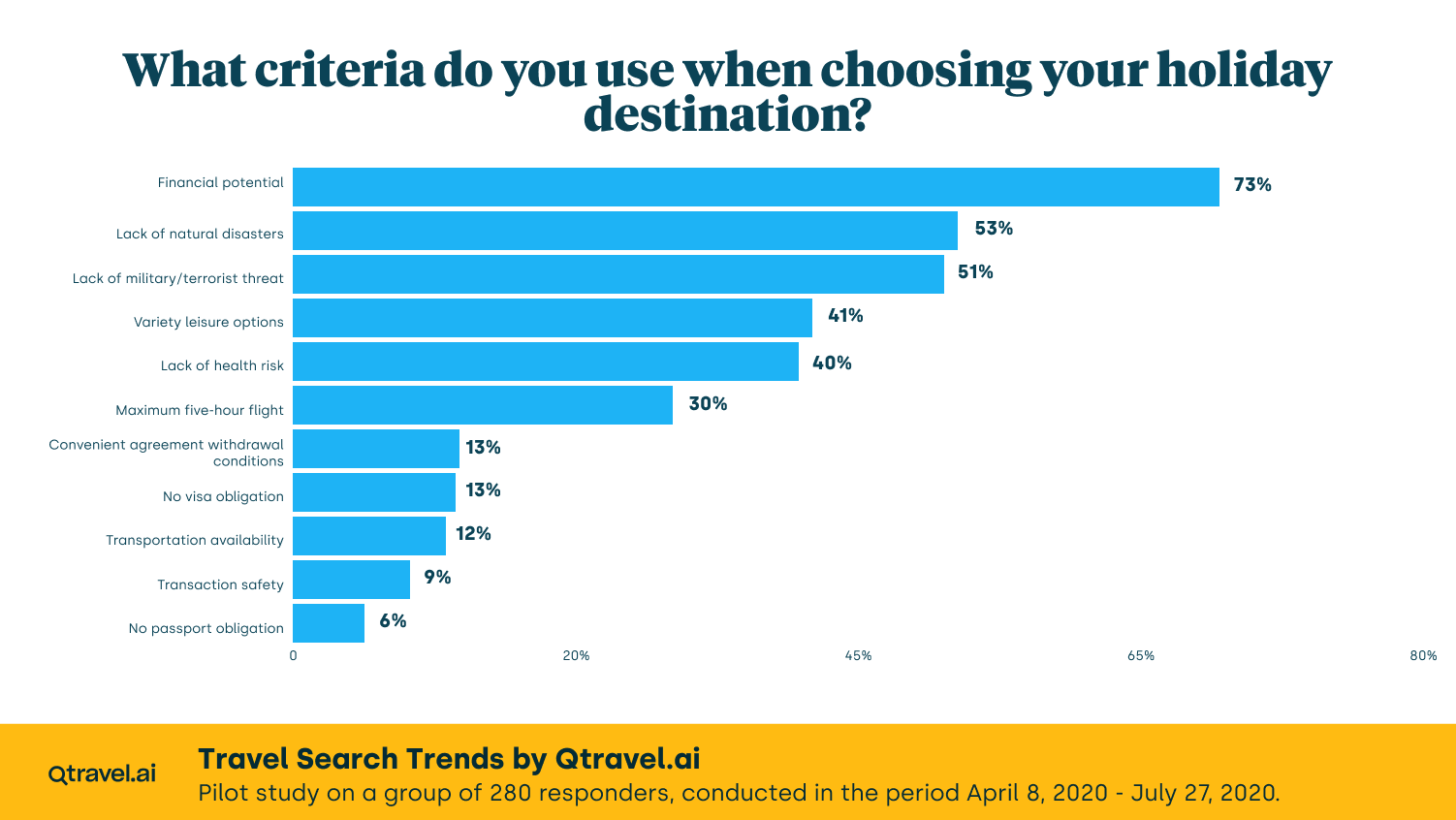

This time we will start with the criteria for choosing holiday destinations. Chart 1 provides an overview of the most frequently selected options (respondents could indicate several answers). Financial capabilities are unquestionably the most important criterion, indicated by as many as 73% of respondents. Interestingly, this answer was selected both by tourists who go on long holidays (two weeks or longer) and those looking for short breaks (e.g. with only one night’s stay). Financial availability is equally important for those who take a solo trip, as well as romantic trips for two, family trips or trips with a group of friends (these aspects were mentioned in the previous part of the series Travel Search Trends 2020. Part 4 – Poles travelling abroad. In each case, the option ‘financial possibilities’ was selected by 70% to 76% of the respondents, which constituted a dominant part of the respondents).

The only exception is the search for a correlation between the significance of financial availability and the primary reason for travelling abroad: those travelling for business purposes ticked this option in only one in ten cases. This confirms the results of almost all surveys related to demand in tourism – business tourism has the lowest price elasticity coefficient. This is because, first of all, the cost of such trips is charged to the employer or is included in business expenses, rather than charged to the budget of the household. Secondly, the fulfilment of professional matters cannot be made dependent on price conditions, although undoubtedly the cost of such trips (especially air tickets) is conducive to business, however, never to such a great extent as in the case of leisure travel.

While the importance of financial issues seems obvious, especially in relation to the tourism of Poles, the following two criteria are rather surprising (the order in Chart 1 is consistent with the number of indications). In earlier surveys from the 2000s, the number of indications for factors related to safety was more than 50 percent lower than for financial accessibility. The survey in question shows a giant shift: more than half of the respondents indicated the exceptional importance of the travel safety factor as one of the most important when choosing a destination. As many as 53% of the respondents allows for natural security (e.g. natural disasters) and 51% – military/terrorist security factors. A leap in these areas occurred after 11 September 2001 (in relation to military security) and after the tsunami in Thailand in 2004 (in relation to natural disasters).

This survey was conducted at an early stage of the COVID-19 pandemic, so the slightly lower position of the category relating to health security (the absence of threats in this area is crucial for 40% of respondents) should not come as a surprise. The first signs of raising awareness in the area of health security occurred after the SARS epidemic in 2002, and the COVID-19 epidemic will further reinforce these tendencies. It is worth stressing, however, that epidemic factors do not discourage travel, but strengthen interest in the scale of preventive measures (sanitary standards) and the possibility of withdrawal from the contract. The current (June 2021) interest in travelling abroad among Poles does not show the slightest downward trend, while enquiries about the conditions of departure are always combined with a search for information on possible refunds in the event of a reinforcing protection of international travel.

A very high position on the list of criteria for selecting the destination is held by the variety of possible options for spending time during the holiday (this category was indicated by 41% of respondents). This means that Poles increasingly expect a flexible approach to their needs in this area: even if the choice concerns a stay by the sea, which seemingly could be limited to good cuisine and a beautiful beach, we like to have in store the possibility of sightseeing, participating in cultural events, trying out new sports and physical activities, personal development, etc. This is not only an important tip for foreign tourism organisers, but also for Polish holiday resorts and leisure facilities. The days when lying on a beach for two weeks satisfied all tourists’ expectations are long gone. The increased value of leisure time, which is related to our being overworked, makes us want to celebrate our holidays and time with the family and friends as fully as possible, and the ‘productivity’ constraint influences our approach to spending leisure time. We are supposed to be resting, but we want to feel that every hour of our holiday brings new experiences, preferably unusual, impressive, and surprising. This is a completely new trend, strongly linked to the popularity of social media. Tourism has always been subject to so-called ‘conspicuous consumption’ and the demonstration effect has strongly driven the industry since its beginning. However, the ability to instantly demonstrate to our friends what we are doing and what great activities we are involved with makes leisure inactivity a waste of time – endlessly sharing photos of yourself on a blanket on the beach, especially if others have learned to paraglide, scuba dived for the first time, or mastered some magic cooking trick, seems a little out of place.

Another important change is the fact that we are increasingly boasting, not so much about the exoticism of places and the number of countries visited, but about the quantity and quality of experiences (in the spirit of experience tourism). In this area, travel operators still have a lot to do, both in the area of the product itself and its sale (marketing communication). Many travel agencies are stuck in the old paradigm, in which luxury was understood as an expensive hotel, a distant trip, or ostentatious exoticism. Today, emphasis should be placed on a different image of luxury: uncommonness (e.g. a night under a starry sky on the roof of a luxury hotel), interesting challenges (e.g. new skills), places unavailable to mass tourism, surprising forms of accommodation (ice cave, glamping, a house in a tree canopy).

An important criterion for foreign travel is the selection of places that can be reached in less than a five-hour flight (one third of respondents chose this answer). Here the correlation with the length of stay seems significant – people who choose shorter stays always marked this option. However, in the group of respondents who undertake long trips (2 weeks or longer), this option was indicated much less frequently, which seems fully understandable. A longer stay compensates for the time of a long flight.

One should also remember about such troublesome issues as the visa requirement or difficult transport accessibility: in the first case 13% of the respondents indicated that while choosing the destination they try to go to countries where a visa is not required, and 12% of the respondents are guided in their choices by convenient transport accessibility (there was almost 100% correlation with the group of people who travel with children in this respect, which is completely understandable).

In the case of travels abroad the most frequently chosen means of transport is of course air transport (this option is indicated by 90% of respondents) and their own car (70% of respondents). Respondents indicated bus and train transport much less frequently (10% each).

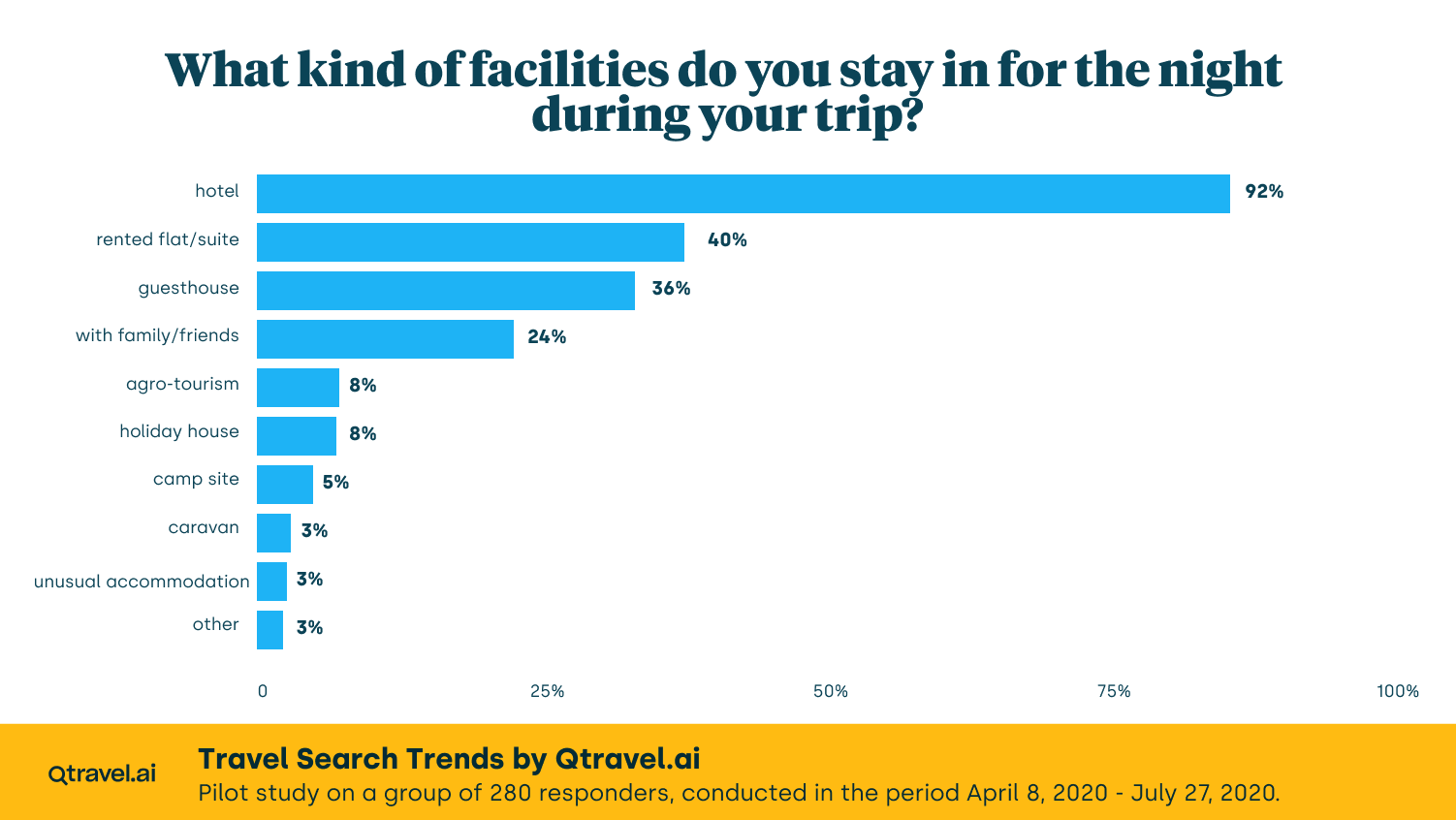

The results of the survey regarding tourists’ preferences for accommodation when travelling abroad are not surprising either. Most respondents trust categorised facilities – primarily hotels – with 92% of respondents selecting this option. The number of people willing to rent flats/suites (40%) or guesthouses (36%) during their stays abroad is less than half. Nearly a quarter of respondents indicated that they stayed abroad with family or friends.

Other forms of accommodation were indicated much less frequently – among them agro-tourism and holiday homes (8% each), camping sites (5%) and caravans (3%). Only 3% of respondents indicated other, non-traditional forms of accommodation. Among yachtsmen it was natural to indicate a yacht/sailing boat as a place of accommodation, but this group of respondents was not numerous, as they use organised recreation much less frequently.

In the next part of the series we will take a look at how and how much in advance holidaymakers plan their holiday trips.

We encourage you to read the rest of the articles in this series:

- Part 1: Profile of the respondents.

- Part 2: How often do tourists travel during the year?

- Part 3: Do we like long holiday stays in Poland?

- Part 4: Poles travelling abroad part 1.

- Part 5: Poles travelling abroad part 2.

- Part 6: How far in advance do we plan tourist trips?

- Part 7: How far in advance do we plan tourist trips? – the income factor.

- Part 8: Flexibility in holiday travel planning.

- Part 9: Frequency of travel versus flexibility in travel planning.

- Part 10: Gender versus flexibility in travel planning.